We live in the era of a rapidly evolving global economy when fintech companies are massively adopting cashless and virtual payment technologies. As the internet is about to undergo a revolution facilitated by 5G and open data formats, Artificial Intelligence and Machine Learning capabilities will significantly expand, blockchain technologies will be improving as never before.

Web 3.0 is expected to bring an improved version of the internet we use today, thus changing our ordinary working processes and collaboration. With Web 3.0, centralized data categorization and storage will be of no use, blockchains will help secure and store data on this decentralized network.

In this article, we are going to explore the possibilities that Web 3.0 will bring. Transformation is coming to financial services, capital markets, asset management, consumer, and wholesale banking. And a new era in technological history will begin.

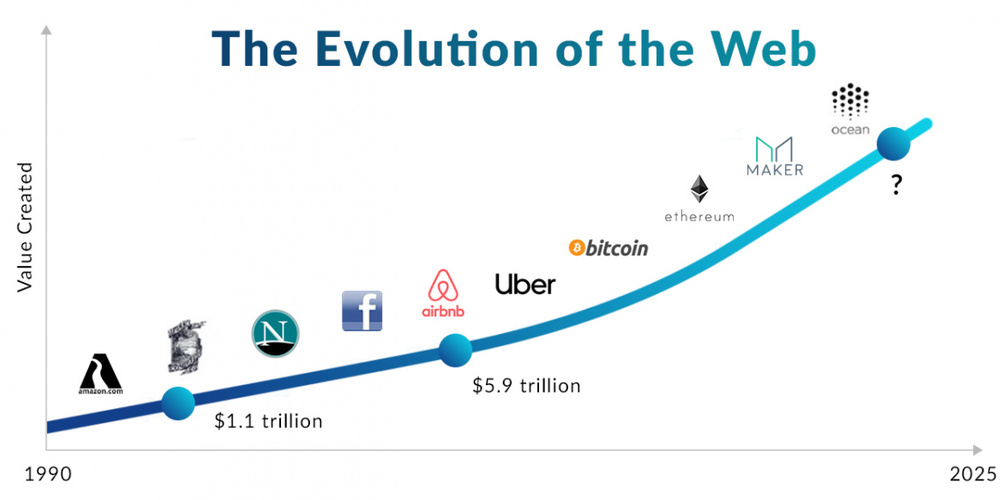

Web 1.0 and Web 2.0

In the 1990s, the first version of the World Wide Web (Web 1.0) allowed the majority of users to view content on static pages with the following characteristics:

- The server’s filesystem was a source of content

- Common Gateway Interface was a tool for building pages

- Frames and Tables helped to design the page

Web 2.0 (the 2000s) significantly changed the way digital information is created, distributed, stored, and used. Thanks to Web 2.0, which brought us user-generated content, usability, and interoperability, we now see the internet as a place for interaction and collaboration.

To be precise, Web 2.0 refers to individuals connecting and sharing information online, like on Myspace, Facebook (before becoming Meta), YouTube, and even Wikipedia. The main characteristics of Web 2.0 include:

- Web-based apps anywhere

- Simple solutions to specific issues

- Value in content, not display software

- Bottom-up distribution, not top-down

- Employees and customers can access and use tools independently

- Information creation, collaboration, editing, categorization and sharing

With the rise of FinTech, insurtech, and regtech, we are seeing a shift in how financial services are sold and consumed. It's not just challenger banks and neobanks vying for the modern financial services consumer. In fact, the worldwide online banking industry is set to explode. It was worth $11.43 billion in 2019 but is expected to hit $31.81 billion by 2027, increasing at a 13.6 percent CAGR.

How Web 3.0 is beneficial?

1. Reliability. Web 3.0 will unleash content creators more broadly. Using decentralized networks, Web 3.0 will give consumers complete control over their online data.

2. It is for all. Web 3.0 can be controlled by several parties. As larger firms may lose control of the internet, decentralized applications (dApps) can therefore not be banned or controlled in any way.

3. Internet personalization. Web 3.0 will be able to recognize user preferences and allow them to customize their web browsing experience, which will also improve your web surfing efficiency.

4. Improved marketing. With Web 3.0's artificial intelligence (AI), sellers can understand your buying preferences and present products and services that users would like, thus allowing us to view better and more relevant adverts.

5. Less disruption. Decentralization prevents account bans and service outages due to technical or other causes because all data is kept on distributed nodes.

Web 3.0 and financial services

As Web 3.0 is more decentralized and individualized than the current internet, what does this mean for finance? While FinTechs got used to rapid market changes, regulations and digital transformation, banks and other traditional institutions will have to catch up and collaborate innovative FinTechs. It means that financial organizations should actively invest in their own technological capabilities.

We see many examples of financial organizations employing AI to increase income, reduce costs, and automate repetitive operations. Most financial experts are optimistic about the potential of AI in financial services. In a recent NVIDIA survey, 83% of finance professionals believed that AI is critical to their company's future success.

The Royal Bank of Canada is leveraging millions of data points to train its own AI, resulting in fewer client calls and faster application delivery. Meanwhile, BNY Mellon, the world's largest cross-border payments service provider, improved its fraud prediction accuracy by 20%. By crunching real-time market data within nanoseconds, AI and high-performance computing (HPC) are combining to provide better and faster trading intelligence.

DeFi might play a much bigger role if Web 3.0 is decentralized and uses blockchain technology. Presumably, centralized finance (CeFi) and DeFi will eventually unite. Companies who actively try to bridge the gap between CeFi and DeFi will lead the way in financial services innovation. So, how does DeFi work? For services, DeFi leverages cryptocurrency and smart contracts, not financial institutions. In DeFi, a smart contract removes the reliance on a financial institution. A smart contract is programmed to send or refund money from one account to another without the involvement of a financial institution.

Capital markets

Cryptos are digital assets that let users transact directly without a payment service provider in the intermediary, which means that they enable new forms of capital. Although Bitcoin remains comparatively low at the moment, it still may provide effective money governance by preserving and protecting the data or memory of what our money represents. Then there is the unparalleled manipulation of fiat money. We can observe how central banks have significantly extended their balance sheets since the GFC and the ongoing pandemic COVID-19. Large-scale money production will undoubtedly distort the true worth of our money.

Bitcoin has provided digital property rights for web content creators earlier. Bitcoin can still secure Web 3.0 applications if it regains its value (cryptocurrencies use the same technologies as Web 3.0 apps). The artificial distinction between money and data will be erased, allowing for the emergence of a united digital society.

Conclusion

Undoubtedly, Web 3.0 will open up new markets, business models, and other unknown prospects. It might entail a “return to the global village”. As Blockchain will be fundamental to Web 3.0, the convergence of revolutionary technologies will be seen, which will elevate the internet to such a level of efficiency as never seen before.

The financial sector will be affected as well. Web 3.0 will create new markets and client segments. COVID-29 has already proven that innovation and tech adoption are critical to survival, so organizations must be ready to accept change and realize the benefits of Web 3.0.

Web 3.0 maintains digital speech freedom, which is quite different from Web 2.0. The next round of decentralization will supposedly return control of a network to users. While it sounds hopeful, it requires responsibility and may prove difficult for both organizations and individuals. Web 3.0 is coming, bringing new opportunities. We'll probably be talking about Web 3.0 in a few years, but we need to be ready to participate and benefit from it.

Source: financialit.net