.png)

The ship recycling market has been under pressure for quite some time, marking 2022 as a rather turbulent year. In its latest weekly report, shipbroker Clarkson Platou Hellas said that “, there is some renewed hope that the financial restrictions experienced in Bangladesh and Pakistan could soon be lessened. It is reported this week that a few recyclers have managed to open Letters of Credit, albeit smaller capital in Bangladesh, which could help the market move into a positive mode as we head into the New Year to finally create some much-needed competition to their counterparts in India. India remains the most stable of the three recycling destinations in the Indian sub-Continent with inquiry to purchase tonnage prominent to attempt to fill their ever-depleting yards. 2022 has been an intriguing year for ship recycling but 2023 certainly looks to have increased supply to the industry. Actual sales during 2022 were considerably down from 2021”.

The shipbroker added that “in relation to the actual dwt committed, the tanker sector supplied about 60% less tonnage for recycling compared to 2021, on the dry bulk side, about 23% down compared to 2021 and around 50% down for all other types of vessels. The container sector continues to struggle in terms of charter rates and the expectancy is to see more container tonnage circulate into the market during next year and more abundantly 2024. Supplies of tanker tonnage will remain at a low whereas we do expect to see more dry bulk tonnage come for sale throughout the year”, Clarkson Platou Hellas concluded.

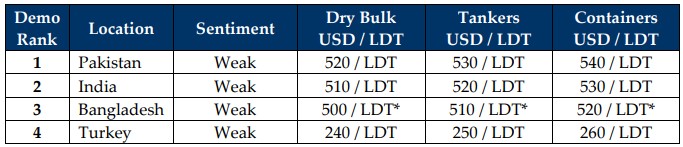

Meanwhile, in a separate note this week, GMS (www.gmsinc.net), the world’s leading cash buyer of ships aded that “as sub-continent markets veer through the last couple of weeks towards the end of the year, we can look back and reflect on what has been an extremely turbulent 2022. Prices reached decade long peaks above USD 700/LDT in the first quarter of the year before crashing back down by about USD 200/LDT, with certain trades seeing below the USD 500/LDT barrier and even into the high USD 400s/LDT on certain occasions. On the West End, the situation was no different in Turkey, where levels too hit a record USD 500/Ton for a brief period, only to plummet about half in value (about USD 250/MT) in a rather short period, and has remained on the sidelines ever since. Steel plate prices and especially the relevant currencies have all seen record lows against the U.S. Dollar, shattering records by the month during the summer period. We have also seen decade lows in the supply of tonnage, with almost all freight sectors performing strongly this year, as we finally seen a much-anticipated rebound on tankers following a number of years in the doldrums.

Dry Bulk and Containers have also had outstanding years, with minimal scrapping seen in both sectors during the first half of the year. As such, moving into 2023, we do expect to see more vessels enter the market for recycling from each of these sectors, especially as freight rates have cooled off considerably towards the end of this year. There are also a number of vessels trading right up to their limits (in terms of surveys) and due to older age profiles and reduced earnings, Owners are unlikely to pass further surveys and may well scrap with recycling rates still looking relatively firm (USD 350/LDT being the historical average). A reduction in the fleet size amidst relatively low newbuilding deliveries for 2023 should help charter rates recover and for various earning cycles to start again”, GMS concluded.

Source: hellenicshippingnews.com